ANNUAL REPORT

2015

By nearly every measure, 2015 was another great year for Travelers. Our 2015 results mark the latest in a decade-long run of industry-leading financial success, and they suggest an outlook for our future that is similarly bright.

We owe the strength of our position to the collective efforts of more than 30,000 people who execute in the marketplace every day, but also, in no small part, to the man I was humbled to succeed as CEO, Jay Fishman.

More than a decade ago, Jay and the senior management team laid out a clear, simple and unwavering mission for creating shareholder value:

Delivering superior returns has been our North Star, and the results are clear. Over the last decade, we produced an industry-leading return on equity, returned over $35 billion of excess capital to our shareholders, grew dividends per share at an average annual rate of 10%, more than doubled our book value per share and delivered a total return of approximately 225% to our shareholders.

Travelers hasn’t simply succeeded from a financial perspective. It is a place where people love to work, a valued partner for our agents and brokers, a source of peace of mind for our customers and a thought leader for the industry. Since Jay announced that he would be stepping down as CEO due to health reasons, many of us have paid tribute to him in our own ways. No one is more pleased than I am that Jay will continue in a key management role as Executive Chairman of the Board. But as a company, I believe our most fitting tribute to Jay’s leadership is to carry forward the success he made possible, and to turn today’s summit into tomorrow’s base camp.

This past year’s terrific results are an ideal place from which to begin that climb.

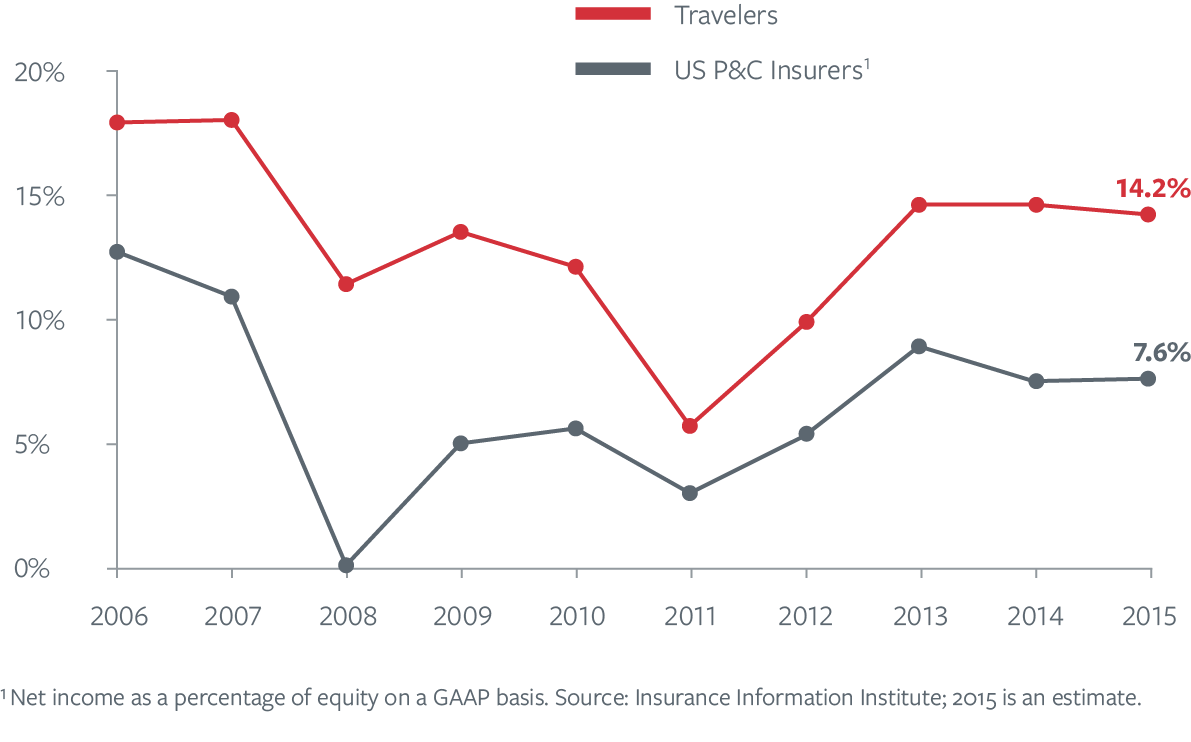

In 2015, Travelers posted record net income per diluted share of $10.88, net income of over $3.4 billion and a strong return on equity of 14.2%. We delivered outstanding underwriting results across our business segments, with a consolidated combined ratio of 88.3%, demonstrating our continued focus on underwriting excellence and the value of industry-leading data and analytics, which have been decades in the making and are continually improving. Our high-quality investment portfolio continued to contribute reliably to our results despite stubbornly low interest rates and more challenging capital market conditions.

We delivered these financial results by successfully executing our marketplace strategies. In domestic Business Insurance, we achieved a record level of retention and positive renewal rate change, consistent with our objectives given the attractive levels of current product returns. In Bond & Specialty Insurance, we generated a very strong combined ratio of 67.9% for the year. Our sustained strong performance in Bond & Specialty Insurance, a set of credit-sensitive businesses, demonstrates our expert management of risk and reward over time and through difficult business environments. In Personal Insurance, the continued success of Quantum Auto 2.0® drove 8% growth in our Agency Automobile policies-in-force count for the year, with retention up by more than two full points and new business up nearly 40% over the prior year. Success in the Auto product also had a positive impact on our top line Homeowners results. Moreover, our success in Personal Insurance was not limited to the top line, with Agency Auto and Agency Homeowners posting full year combined ratios of 94.7% and 75.8%, respectively. All in all, this excellent execution across our businesses contributed to record consolidated net written premiums of just over $24 billion in 2015.

Finally, our earnings and significant cash flow enabled us to continue to invest in our businesses while at the same time returning excess capital to our shareholders, increasing book value per share and maintaining our balance sheet strength. During 2015, we returned over $3.9 billion in capital to our shareholders, comprising more than $3.2 billion in share repurchases and $744 million of dividends. We also increased our dividend per share by 10.7%.

The results we deliver are due to our deliberate and consistent approach to creating shareholder value. We have been clear for many years that one of our crucial responsibilities is to produce an appropriate return on equity for our shareholders. This has meant developing and executing financial and operational plans consistent with our goal of achieving superior returns, which we defined many years ago as a mid-teens operating return on equity over time. We emphasize that the objective is measured over time because we recognize that interest rates, reserve development and weather, among other factors, impact our results from year to year, and that there are years — or longer periods — and environments in which a mid-teens return is not attainable and other years in which we expect we will achieve or exceed a mid-teens return. In that regard, we established the mid-teens goal at a time when the 10-year Treasury was yielding around 5%, and in that environment, a mid-teens return was industry leading. As we’ve said before, our ability to achieve a mid-teens return over time going forward will depend on interest rates returning to more normal levels by historical standards. In any event, we will always seek to deliver industry-leading, superior returns over time.

Our focus on operating return on equity encompasses multiple performance objectives that are key to creating shareholder value. The measure is a function of both (1) operating income and (2) shareholders’ equity (excluding unrealized gains and losses on investments). Accordingly, operating return on equity reflects a number of separate areas of financial performance related to both our income statement and balance sheet, including the quality and profitability of our underwriting and investment decisions, the pricing of our policies, the effectiveness of our claims management and the efficacy of our capital and risk management.

Our average annual operating return on equity over the last decade is 13.8%, a meaningful spread over the average 10-year Treasury and meaningfully in excess of our average cost of equity, in each case for that period. In addition, as demonstrated by the chart below, our return on equity has meaningfully exceeded the average return on equity for the P&C industry in each of the last 10 years.

One critical component of our ability to deliver exceptional returns over time is our granular approach to underwriting. In our commercial businesses, that means execution, including the allocation of capital, on an account-by-account or class-by-class basis. In personal lines, that means a very high degree of account segmentation and the allocation of capital generally on a very local geographic basis. With that and our advanced data and analytics, we select the risks we write and price our products deliberately with our targeted return in mind.

In addition, as we have said for some time, we are believers that the amplitude of the “pricing cycle” in our industry does not exist to the same degree as it had in the past. While we’re not immune from market conditions, we are also not passive rate takers. For us, this means that we don’t let the notion of a pricing cycle deter us from deliberate execution.

Overlaying all of this is a culture that understands how to balance the art and science of decision making based on data and analytics. That culture alone is a competitive advantage, and one that we believe is hard to replicate.

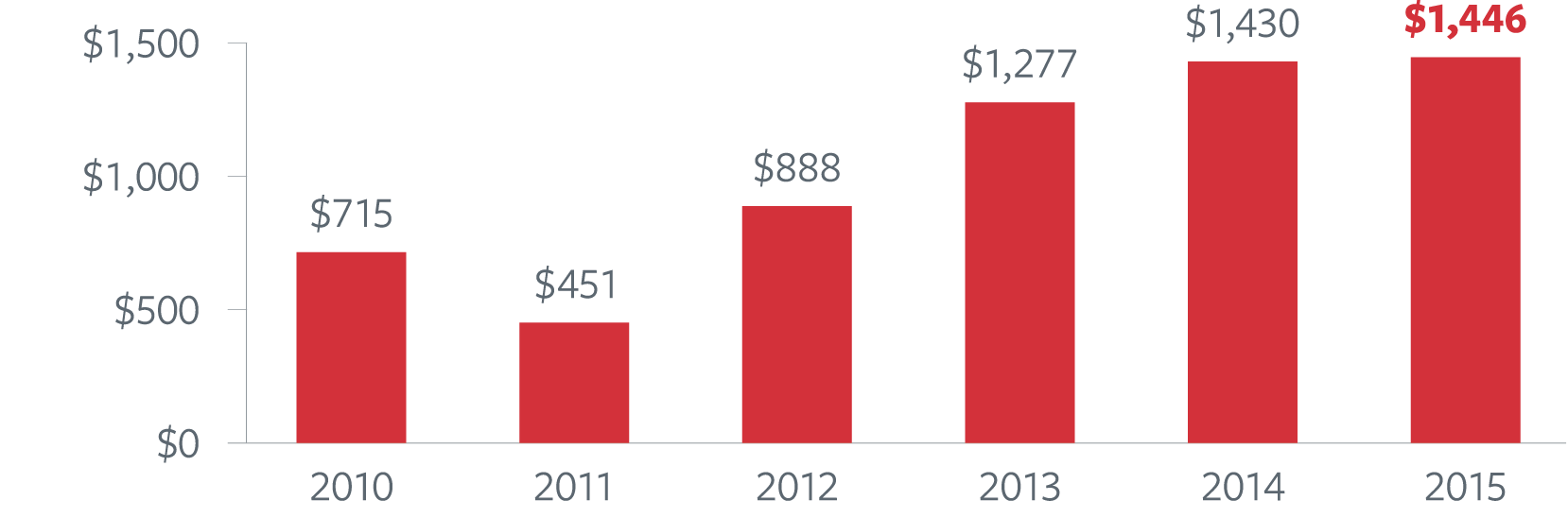

You can see the success of our granular and deliberate strategy in the chart below, which shows our after-tax underlying underwriting margin, which is our underwriting margin excluding the impact of catastrophes and net favorable prior year reserve development, for each year since 2010.

Just as a data point, our after-tax net investment income is about $1 billion lower in 2015 as compared to its recent high in 2007, driven by the low interest rate environment. On the other hand, our after-tax underlying underwriting margin is about $1 billion higher in 2015 than it was at its recent low in 2011. With capital increasingly finding its way into that portion of the business that serves the largest and most global accounts, and with interest rates as low as they currently are, our expertise in generating underwriting margins and our strong franchises in the small and middle marketplaces with meaningful barriers to entry really matter.

Our granular and deliberate execution goes beyond risk selection and pricing. There are other profitability levers in our business, including volume, mix, expenses and reinsurance. We have a long track record of capitalizing on all of the available levers to deliver superior returns – and of applying these levers on a strategic and business-by-business basis. This is evident in the way we have executed quite differently in each of our business segments over the past several years.

Our ability to assess, diagnose and execute gives us great confidence in our ability to outperform the competition going forward, regardless of what the future brings.

Similar to our underwriting strategy, our investment philosophy is well defined and consistent. Our investment portfolio is managed first and foremost to support our insurance operations and, accordingly, is positioned to meet our obligations to policyholders under a wide range of conditions. We emphasize risk-adjusted returns and credit quality rather than reaching for yield that is not consistent with the underlying risk. Our asset allocation is designed so that even when we experience lower non-fixed income returns, which we know on occasion we will, the predictable stream of investment income from our fixed income portfolio will nonetheless provide a firm and reliable foundation for our overall results. That’s exactly what we saw in 2015, and that’s our investment philosophy at work – it’s not an accident.

Our performance has enabled us to return significant amounts of excess capital to our shareholders in the form of dividends and share repurchases while meaningfully growing book value per share. We set our dividend at a level that we believe to be both competitive and sustainable, recognizing that we provide coverage for catastrophic events, and use share repurchases to return additional excess capital to our shareholders. This strategy gives us the flexibility to respond to changing business conditions and permits us to take advantage of business opportunities as they present themselves.

Our capital management strategy has been an important driver of shareholder value creation. Since the initial share repurchase authorization granted by our Board on May 2, 2006, and through the end of 2015, we have returned over $35 billion of capital to our shareholders through share repurchases and dividends, more than 100% of the company’s market capitalization on that day. Importantly, over the same period, book value per share grew by a compound annual growth rate of more than 9%.

Since the announcement of my appointment as CEO, I’ve been asked many times about my approach to acquisitions. Our approach has not changed. The lens through which we evaluate acquisition opportunities — which, as our shareholders should expect, we do all the time — is that a transaction should contribute to our mission by improving our long-term return profile, reducing the volatility of our returns or creating shareholder value through some other important strategic benefit, such as a geographic or product position.

We have a great deal of experience in executing strategic transactions, and we view this as a core competency. The company that we are today has come together through a number of significant transactions over the past two decades. More recently, we have expanded our operations in Canada through the acquisition of Dominion, made a joint venture investment in the leading surety business in Brazil, established a presence in the property and casualty insurance market in Brazil and, through our Brazilian surety joint venture, invested in a start-up surety business in Colombia.

While we have an international footprint and the ability to place our customers’ business all over the world, we are primarily U.S. based. Given that the United States is the largest insurance market in the world, along with the current outlook for economic instability and geopolitical risk in so many regions outside the United States, our current geographic position is very attractive. Nonetheless, over the past five years or so, we have invested in our capability to deliver our competitive advantages outside of the United States, and we are prepared for opportunities as we find them. We’ll proceed thoughtfully and deliberately, maintaining our discipline and pursuing only those opportunities that we are confident will meet our objectives.

Ultimately, the success of our strategy — with all its component parts — drives our superior total returns to shareholders over time.

In contrast to many other property and casualty companies, our level of shareholder returns over recent years reflects consistent strong performance rather than a recovery from a significant decline during the financial crisis.

I couldn’t be more confident that maintaining the approach we have followed for more than a decade is the right strategy to continue to build on Travelers’ outstanding record. It’s part of our DNA, we understand it, we’ve been executing it and it has been remarkably successful.

In an industry like ours, it’s essential to look beyond our four walls at the changes taking place across the economy in order to stay competitive. The speed, scale and scope of innovation taking place right now are unprecedented, and it’s important to consider how these trends will affect our industry over time.

I am quite optimistic about how we will perform in this environment. Innovation is a hallmark of our great company, and we’ve never been intimidated by change. We issued the first auto insurance policy and the first travel insurance protection for astronauts. In 1955, we pioneered a homeowners policy that combined fire, theft and liability coverage, which 61 years later is still the industry standard. In 1997, we issued the first insurance policy to protect individuals using personal computers for online banking.

More recently, we have been at the forefront of data and analytics, leading in an area that has come to dominate our entire industry. We’ve continued this long-standing focus on innovation – from the launch of Quantum Auto 2.0 to our workers compensation business, where we have introduced ConciergeCLAIM® Nurse and predictive modeling for chronic pain.

These efforts by the most dedicated and creative talent in this industry enable us to stay at the forefront, delivering innovative products and solutions to our customers, giving them more reasons to choose Travelers – and to stay with us once they do. We are confident that, moving forward, we will continue to be well positioned to find and capitalize on the opportunities that a changing world will inevitably present.

We’re proud of our nearly $200 million in philanthropic giving over the past decade. To us, this is about more than writing checks and making grants. Central to Travelers’ identity is that we have a responsibility to give back to the communities where our employees, customers and agents live and work. It’s also about encouraging and fostering real and lasting employee engagement in our philanthropic priority areas: academic and career success, thriving neighborhoods and arts and culture.

In 2015 alone, 3,675 members of the Travelers family logged more than 90,000 volunteer hours – a 30% increase over 2014. From Habitat for Humanity, to our Small Business Risk Education Program, to our mentorship and scholarship programs benefiting students at all levels, we’re committed to creating opportunities and then to helping people make the most of them. This is the right thing to do. But it also happens to be the smart thing to do, because a commitment to community strengthens our company in the long run. Whether you act from your head or your heart, you come to the same conclusion.

Another illustration of our civic-minded, outward-looking identity is the public policy work we undertake, including through our policy organization, the Travelers Institute®. Our industry touches so many others, and our business is often subjected to global trends and national issues ranging from economic growth to regulatory regimes. Some of these we can’t influence, and we must simply prepare for them. In other areas, we do have the ability to advise and perhaps even influence policy. In all cases, our policy work is unique, and uniquely important.

From small business advocacy, to disaster preparedness and consumer insurance education symposia, to work that engages policymakers and regulators in policy dialogue, we believe that with industry leadership comes responsibility, and we endeavor to advance the thinking that’s advancing our industry. We’re committed to being a go-to and trusted source of information and insight, and we seek to influence public policy in the interest of the common good.

One of the areas in which we have been and will continue to be vocal is regarding threats to the competitiveness of our domestic insurance industry. Specifically, we continue to see the U.S. corporate income tax rate — the highest of any industrialized nation — as encouraging insurers to shift capital offshore, ultimately harming the U.S. economy. Ensuring that U.S. companies remain competitive should be a priority for Congress.

As we look forward, it’s clear that a decade of thoughtful, diligent management has put us in an excellent position to continue our strong performance in the years ahead. At a moment when many others in the industry are struggling with a variety of challenges, we are in a position to innovate and lead.

In the years ahead, in large part by maintaining our effective strategy and continuing to invest in our competitive strengths, we intend to press our advantages. We’ll leverage our lead in data and analytics and solidify our leadership in risk selection and pricing. We’ll keep innovating across our products and throughout our world-class Claim and Risk Control organizations to keep our agents, brokers and customers on the cutting edge. And we’ll maintain our distribution partner advantage to make sure we remain a partner of choice.

In the months since I succeeded Jay, people have asked me what it’s like to follow a legend. I tell them that, fortunately for me, Jay set the stage for Travelers’ future achievements. He has perpetuated a culture of hard work, collaboration, high standards, mutual support, innovation and constant improvement. In that sense, Jay’s legacy is far more than a decade of success in the books. It’s also a culture that will enable us to achieve the next decade of success.

I’m enormously grateful to every person who worked tirelessly to deliver this past year’s exceptional results. Travelers’ success is possible because of the counsel and commitment of our Board of Directors, the dedication and passion of every Travelers employee, the partnership and insights of our agents and brokers and the loyalty of so many of our customers. It is my privilege to work with all of you toward even better years to come.

At and for the year ended December 31. Dollar amounts in millions, except per share amounts.

| 2015 | 2014 | 2013 | 2012 | 2011 | |

| Earned Premiums | $23,874 | $23,713 | $22,637 | $22,357 | $22,090 |

| Total Revenues | $26,800 | $27,162 | $26,191 | $25,740 | $25,446 |

| Operating Income | $3,437 | $3,641 | $3,567 | $2,441 | $1,390 |

| Net Income | $3,439 | $3,692 | $3,673 | $2,473 | $1,426 |

| Net Income Per Diluted Common Share | $10.88 | $10.70 | $9.74 | $6.30 | $3.36 |

| Total Investments | $70,470 | $73,261 | $73,160 | $73,838 | $72,701 |

| Total Assets | $100,184 | $103,078 | $103,812 | $104,938 | $104,575 |

| Shareholders’ Equity | $23,598 | $24,836 | $24,796 | $25,405 | $24,477 |

| Return On Equity | 14.2% | 14.6% | 14.6% | 9.8% | 5.7% |

| Operating Return On Equity | 15.2% | 15.5% | 15.5% | 11.0% | 6.1% |

| Book Value Per Share | $79.75 | $77.08 | $70.15 | $67.31 | $62.32 |

| Dividends Per Share | $2.38 | $2.15 | $1.96 | $1.79 | $1.59 |

The Travelers Companies, Inc. (NYSE: TRV) is a leading provider of property and casualty insurance for auto, home and business. The company’s diverse business lines offer its customers a wide range of coverage sold primarily through independent agents and brokers. A component of the Dow Jones Industrial Average, Travelers has approximately 30,000 employees and operations in the United States and selected international markets.

| 2015 | High | Low | Cash Dividend Declared |

| First Quarter | $109.73 | $102.82 | $0.55 |

| Second Quarter | 108.67 | 96.14 | 0.61 |

| Third Quarter | 107.82 | 97.49 | 0.61 |

| Fourth Quarter | 115.83 | 98.34 | 0.61 |

| 2014 | High | Low | Cash Dividend Declared |

| First Quarter | $89.33 | $80.26 | $0.50 |

| Second Quarter | 95.60 | 84.39 | 0.55 |

| Third Quarter | 95.95 | 89.12 | 0.55 |

| Fourth Quarter | 106.95 | 91.81 | 0.55 |

| (Dollars in millions, after tax) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 |

| Reconciliation of operating income less preferred dividends to net income | ||||||||||

| Operating income, less preferred dividends | $3,437 | $3,641 | $3,567 | $2,441 | $1,389 | $3,040 | $3,597 | $3,191 | $4,496 | $4,195 |

| Preferred dividends | - | - | - | - | 1 | 3 | 3 | 4 | 4 | 5 |

| Operating income | 3,437 | 3,641 | 3,567 | 2,441 | 1,390 | 3,043 | 3,600 | 3,195 | 4,500 | 4,200 |

| Net realized investment gains (losses) | 2 | 51 | 106 | 32 | 36 | 173 | 22 | (271) | 101 | 8 |

| Net income | $3,439 | $3,692 | $3,673 | $2,473 | $1,426 | $3,216 | $3,622 | $2,924 | $4,601 | $4,208 |

| (Dollars in millions) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2005 |

| Reconciliation of adjusted shareholders’ equity to shareholders’ equity | |||||||||||

| Adjusted shareholders’ equity | $22,307 | $22,819 | $23,368 | $22,270 | $21,570 | $23,375 | $25,458 | $25,647 | $25,783 | $24,545 | $22,227 |

| Net unrealized investment gains (losses), net of tax | 1,289 | 1,966 | 1,322 | 3,103 | 2,871 | 1,859 | 1,856 | (146) | 620 | 453 | 327 |

| Net realized investment gains (losses), net of tax | 2 | 51 | 106 | 32 | 36 | 173 | 22 | (271) | 101 | 8 | 35 |

| Preferred stock | - | - | - | - | - | 68 | 79 | 89 | 112 | 129 | 153 |

| Discontinued operations | - | - | - | - | - | - | - | - | - | - | (439) |

| Shareholders’ equity | $23,598 | $24,836 | $24,796 | $25,405 | $24,477 | $25,475 | $27,415 | $25,319 | $26,616 | $25,135 | $22,303 |

| (Dollars in millions) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 |

| Calculation of average annual operating return on equity | ||||||||||

| Operating income, less preferred dividends | $3,437 | $3,641 | $3,567 | $2,441 | $1,389 | $3,040 | $3,597 | $3,191 | $4,496 | $4,195 |

| Adjusted average shareholders’ equity | 22,681 | 23,447 | 23,004 | 22,158 | 22,806 | 24,285 | 25,777 | 25,668 | 25,350 | 23,381 |

| Operating return on equity | 15.2% | 15.5% | 15.5% | 11.0% | 6.1% | 12.5% | 14.0% | 12.4% | 17.7% | 17.9% |

| Average annual operating return on equity for the period Jan. 1, 2006 – Dec. 31, 2015 | 13.8% | |||||||||

| (Dollars in millions, after tax) | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 |

| Reconciliation of after-tax underwriting gain (excluding the impact of catastrophes and net favorable prior year reserve development) to net income | ||||||

| Underwriting gain excluding the impact of catastrophes and net favorable prior year reserve development (underlying underwriting margin) | $1,446 | $1,430 | $1,277 | $888 | $451 | $715 |

| Impact of catastrophes | (338) | (462) | (387) | (1,214) | (1,669) | (729) |

| Impact of net favorable prior year reserve development | 617 | 616 | 552 | 622 | 473 | 818 |

| Underwriting gain (loss) | 1,725 | 1,584 | 1,442 | 296 | (745) | 804 |

| Net investment income | 1,905 | 2,216 | 2,186 | 2,316 | 2,330 | 2,468 |

| Other, including interest expense | (193) | (159) | (61) | (171) | (195) | (229) |

| Operating income | 3,437 | 3,641 | 3,567 | 2,441 | 1,390 | 3,043 |

| Net realized investment gains | 2 | 51 | 106 | 32 | 36 | 173 |

| Net income | $3,439 | $3,692 | $3,673 | $2,473 | $1,426 | $3,216 |

Average shareholders’ equity is (a) the sum of total shareholders’ equity excluding preferred stock at the beginning and end of each of the quarters for the period presented divided by (b) the number of quarters in the period presented times two.

Adjusted shareholders’ equity is shareholders’ equity excluding net unrealized investment gains (losses), net of tax, net realized investment gains (losses), net of tax, for the period presented, preferred stock and discontinued operations. Adjusted average shareholders’ equity is (a) the sum of adjusted shareholders’ equity at the beginning and end of each of the quarters for the period presented divided by (b) the number of quarters in the period presented times two.

Average annual operating return on equity over a period is the ratio of (a) the sum of operating income less preferred dividends for the periods presented to (b) the sum of the adjusted average shareholders’ equity for all years in the period presented.

Return on equity is the ratio of (a) net income less preferred dividends for the period presented to (b) average shareholders’ equity for the period presented.

Definitions of other terms used in this Annual Report are included in the Glossary of Selected Insurance Terms portion of the downloadable Form 10-K.